Whether you’re an adult going back to school or a new high school graduate, there is a lot to know when you’re thinking about college or career education. One of those is how you should plan on funding your schooling.

You will soon discover the high tuition and the room and board expenses when you start looking at colleges. Even if you are eligible for a scholarship or your family has saved some funds, you may need to turn to other college funding alternatives.

It is here where federal student loans come in. But what are student loans from the federal government, and how do you get them? Further information on this type of loan is available below, so you can make wise decisions when it comes to funding your education.

Federal Student Loans

The federal government gives all eligible college students subsidized student assistance. These loans don’t require a credit check, come with small, fixed interest rates and flexible options for repayment.

If you have to take out college loans, then federal student loans can be your best option.

Federal student loans can be divided into a couple of categories depending on who the applicant is and whether the loan is need-based. The cap and the interest rate of federal student loans rely primarily on the type of loan.

Direct Subsidized Loans

These are need-based loans for financially challenged students. You can only obtain this loan type to fund your entire college when working toward an associate or a bachelor’s degree.

Subsidized loans have an interest rate of 5.5%, and while you’re in school, the government pays the interest. Every year the maximum amount you can borrow is between $3,500 and $5,500.

Direct Unsubsidized Loans

Every college student in the U.S. is entitled to unsubsidized loans. They have an interest rate of 5.5% for undergraduate students and an interest rate of 6.6% for graduate students.

Usually, this is lower than any private loan. Compared to subsidized loans, unsubsidized loans raise interest while you are in school. The maximum amount that you can borrow is from $5,500 to $12,500 per year.

Direct PLUS Loans

Graduate students and college students’ parents can borrow loans from Direct PLUS. These unsubsidized loans have an interest rate of 7.6%.

Your parents could take out a Direct PLUS loan to help pay the remaining costs of your schooling. However, some private lenders might provide cheaper rates.

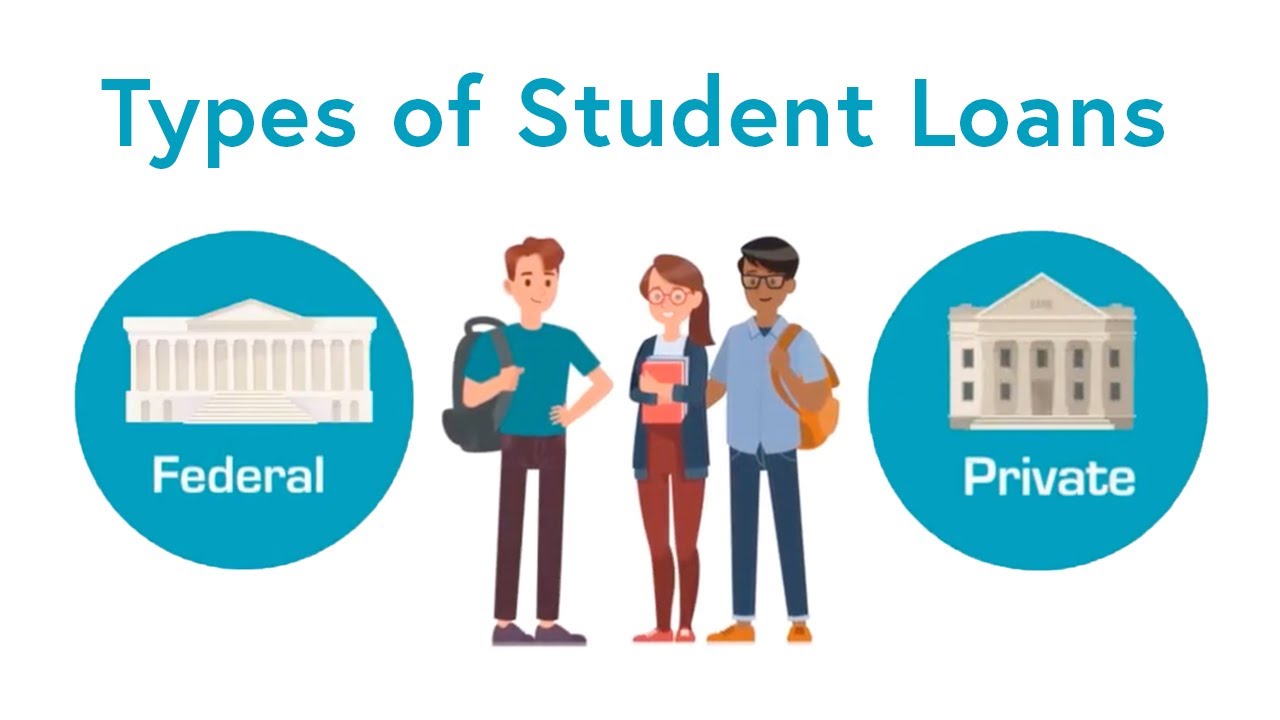

Federal vs. Private Student Loans

When federal loans, savings, scholarships, and grants can’t cover college costs, you might be grappling with how to pay for your education. Private student credits can help fill the gaps.

These student loans are provided by financial institutions such as online student loan companies, banks, or credit unions. Private student loans offer competitive interest rates, as opposed to federal student loans—the healthier the credit score, the lower the interest rate.

But the interest rates are not typically as low as federal rates. If you have no credit, you might need a parent to co-sign the loan. Furthermore, private student loans appear to be less compassionate than federal student loans.

You will have to pay when you are still in school and have no options for repayment. Conversely, even though you have a low salary or go on disability, you would continue to make the same monthly payment. This makes it harder to repay if you venture into a low-earning career.

Bottom Line

If you decide to take on your federal loan application, make sure you understand who is taking the loan and the terms and conditions of the loan. Federal student loans usually have more benefits than loans from banks or other private sources.